2016 is just around the corner, and while you are thinking of your New Year’s resolution of a better diet, more exercise, spending more family time, etc.,don’t forget about your financial fitness. It’s time to take a break from the holiday shopping and eating out, and get your finances in order before the New Year. I’ve always found this time of year a great opportunity to review my portfolio, understand where my spending is going (or NOT), and give my finances a little love. Just like diet, exercise, and physical fitness, financial fitness is something we should do more than once a year. Without reviewing your financial discipline and rigor to understand where you are, it’s difficult to improve and build wealth over time. It won’t happen in one year, but if you keep chipping away at it, month-by-month, year-by-year, you’ll be amazed at what you can accomplish. As I’ve said before, ‘You Can’t Own Everything’, but ‘You Can Own Anything’, if you have a plan and the discipline to stick to it.

Here’s a quick little financial fitness checklist I thought I’d share before the New Year:

7. Evaluate Your Spending

Reviewing a year’s worth of spending all at once can be an eye-opening exercise, but it’s the best way to cut back on all of those little unnecessary purchases that add up throughout the year. If you’re not using a personal finance app, there are quite a few available and most are free. Here’s a link to a useful blog post from our friends at MoneyUnder30.com. Most of these apps come in handy to not just track your spending, but to monitor your investments and calculate your entire net worth.

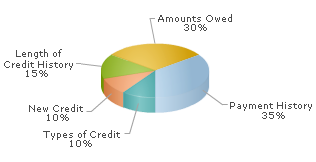

6. Check Your Credit Score

If you’re ever going to want a mortgage, apartment, house, or car, having good credit is crucial. Your credit score can also be used to determine the price you pay for insurance, affect future job offers, etc. Keeping tabs on your credit should be a regular priority, and it’s easy to do through any of the top three credit reporting agencies. The Fair Credit Reporting Act (FCRA) requires each of the nationwide credit reporting companies — Equifax, Experian, and TransUnion — to provide you with a free copy of your credit report, at your request, once every 12 months. Again, it’s free, just takes a little time and discipline on your part to make it happen!

5. Make Charitable Contributions

December 31 is the deadline for contributing to a charitable organization and still being able to deduct it from your taxes, so there is no better time to give back. And remember, contributions don’t have to be cash. You can donate cars, clothing, food, household goods, and even shares of stock. Donating highly appreciated shares of stock from a taxable brokerage account has a triple benefit. It helps your charity, it can provide you a deduction on the full amount if the charity is qualified, and it can avoid capital gains tax on profits. If you don’t have a favorite charity yet, but want to see how effectively a charity uses your donation, check out Charity Navigator.

4. Start Or Fund Your Child’s 529

529 plans are the college savings vehicle of choice for most parents. That’s because they allow contributions to grow free of federal taxes and, in some cases, provide for a state tax deduction, too. In most states, December 31 is the cutoff for annual 529 contributions to be counted in that tax year, so contribute what you can. My wife and I opened up our kids 529 plans the month they were born and have been contributing to them monthly ever since. Our son is now 17, daughter 14, and still not sure if we have enough saved, but 529’s provide a tax savings benefit while establishing a solid foundation for your children’s education over time.

3. Estimate Your 2015 Taxes

You don’t have to file your tax return until April 15, but it’s good to have an idea of what it will amount to by the time the deadline comes around. Try a service like Turbo Tax to estimate your tax, and you’ll be prepared in case you end up owing money to the IRS. It’s better to know now and have 90+ days to prepare if you owe Uncle Sam!

2. Max Out 401k / IRA Contributions

Maxing out your 401k is one of the best ways to reduce your taxes and save more money for your future self. Funds you contribute to a 401k account are pre-tax dollars, meaning they’re taken out of your paycheck before you pay taxes on them. The benefit is that you lower the overall amount of income that you have to pay tax on now, and the money in your 401k can grow tax deferred until retirement. The maximum you can contribute to a 401k account in 2015 and 2016 is $18,000. You can contribute up to $24,000 if you’re 50 or over. If you are in an employer matched 401k, it’s ideal to contribute the maximum amount your employer will match since that’s basically FREE money! If you don’t have an employer sponsored 401k, but have an IRA, hitting the contribution limits on your retirement account goes a long way toward your financial fitness later in life. The limit on both traditional and Roth IRA contributions for 2015 is $5,500 ($6,500 if you’re 50 or older). If you haven’t hit those amounts yet, now is a good time to make a little push to get there. The IRS is actually your friend in this area because you have until April 15, 2016, to make your 2015 contributions, so make a plan now. Again, this is all about financial fitness for life!

1. Rebalance Your Portfolio

Some people know what mix of investments they have when they create their portfolio, but that mix can change over time based on the performance of each type of investment and how subsequent contributions are invested. At the end of the year, see what your investment mix looks like and make any necessary adjustments to better reflect your investment goals and risk tolerance. If you are using a personal finance app that I mention in #8 above, these will usually give you a view of your portfolio mix.

How will you use the end of the year to improve your financial fitness? Do you have financial to-do’s to add to my seven? If so, I’d love to hear them!