Financial fitness and money management generally isn’t a fun topic for most of us--it can be boring, scary, and frustrating. In Fidelity’s recent study, 39% of millennials worry about finances and 25% don’t know who to trust. How do you know if you can afford to go to that music festival with your friends today and not need that money later? Are you aware of where much of your money goes, or how to best allocate it? These are all common questions that potential home buyers have as they start to plan for the future…..Your financial fitness depends on your financial knowledge; so let’s look at 4 financial terms that every homebuyer should know and why:

1. Debt-to-Income Ratio – This is a ratio of your total monthly debt payments divided by your monthly take-home pay or after-tax pay. This is an important ratio to understand when purchasing a home as it’s a key measure for mortgage companies to qualify you for a loan. To qualify for a conventional mortgage, your Debt-to-Income should be less than 45%. For a first time homebuyer, there are programs out there that you can qualify for with up to 55% Debt-to-Income ratio. For example, if your after taxes take-home pay is $5,000/month, all of your monthly debt payments should not exceed $2,250. Your monthly debt payments would include mortgage + car loans + student loans + credit cards + personal loans = $2250 or less.

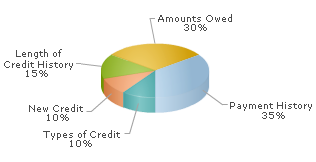

2. Credit Score (aka FICO) - One of the most common ways credit scores are calculated is the FICO method, from Fair Isaac Corporation. A FICO credit score can range anywhere from 300 to 850. FICO credit scores are calculated based on five categories of information:

- Payment history - 35% or 297.5 points

- Amounts owed -30% or 255 points

- Length of credit history - 15% or 127.5 points

- New credit - 10% or 85 points

- Types of credit - 10% or 85 points

The graph below shows the relative weight that each one of these categories has in the calculation of your credit score.

Category Possible Points

Payment history

|

297.5

| |

Amounts owed

|

255.0

| |

Length of credit history

|

127.5

| |

New credit

|

85.0

| |

Types of credit

|

85.0

| |

Totals

|

850

|

Credit Score Ranges

700-850 A "very good" or "excellent" credit score. You should not have a problem getting a loan from a lender.

680-699 A "good" credit score. Though not considered very good or excellent, most lenders will not have a problem giving you a loan.

620-679 An "acceptable" credit score. Lenders will most likely require you to provide supporting information regarding your income, time in your current home, bank statements, time with current employer, etc.

580-619 An "okay" credit score. 620 is the prime rate cut-off point, so you can expect to pay a higher interest rate with any lender who is willing to give you a loan.

500-579 A "bad" credit score. You may still be able to get a loan with a score like this, but you will most definitely be paying a higher interest rate.

350-499 A "very bad" credit score. You can still get a loan with this low of a credit score, but you may be better off turning it down and cleaning up your credit score over the next several years. Otherwise, the interest on the loan may be too difficult to handle.

Generally speaking, you need at least a 620 credit score to qualify for a conventional mortgage. However, there are FHA or first time homebuyer programs out there where you can qualify with as low as a 580 credit score.

3. Assets - Of the “four legs of the table” (Debit, Income, Credit, Assets), assets are the least discussed, and yet may be the most important. Assets are usually categorized into 4 main areas:

- Business Ownership - you own your own business or % of someone else’s business

- Real Estate - primary residence, investment/rental properties, vacation home, etc.

- Paper/Liquid Funds - savings, checking, stocks, mutual funds -

- Commodities - oil, gas, gold silver, etc.

So, your assets include, real estate, cars/boats, checking/savings account, stocks/bonds, money markets, mutual funds, jewelry, etc. Lenders look at your assets to make sure you have the needed down payment (the difference between the purchase price and the loan amount which may or may not be the same as the money deposit at contract signing), but also reserves after closing in case an emergency arises you have the means to continue paying your mortgage. The key areas that lenders look for:

- Monies needed for closing costs (fees to the lender and third parties for things like appraisals, title insurance, settlement services, and so on)

- Monies needed for Pre-Paids (homeowners insurance, flood insurance, real estate taxes, etc.) and establishing escrow accounts for future payments

- Monies for Reserves- the money you still have left after closing. Monies that would be available, if a problem were to arise

How many of these did you already know? Understanding the intricacies of personal finance can give you a huge edge moving forward--especially as you look towards buying that first house!.

Any questions you may have about Real Estate finance terms, let us know and happy to talk you through it. Call us at 855-REC-6700 or email at concierge@reconcierges.com .

No comments:

Post a Comment