You want to build wealth and achieve financial stability, but where do you start? Especially if you’re renting and paying a landlord 25% of your income, how do you get out of the Renter rat race to become an Owner and ultimately an Investor where you are the landlord and achieve Home$mart financial stability? How do you go from living paycheck-to-paycheck to your landlord to building wealth through real estate?

As I was writing this blog, I was thinking back on my experience and how I made the journey to becoming more Home$mart and achieving financial stability. I wanted to share the steps that helped me move from Renter > Owner > Investor > Home$mart. One of the first questions I always get is, ‘Where do I start and what’s my next step?” Here are my thoughts/answers:

Preparing to move from Renter to Owner:

Owning a home is probably the biggest investment/purchase you will make in your lifetime. It’s a big financial decision, therefore you need to have your finances in order to move from Renter to Owner.

Step 1: Understand your financial situation and get on a budget. If you don’t know where your money is going, it’s difficult to work towards Home$mart and financial stability. You can own anything with a 20-30-50 plan. There are some great online tools/resources out there such as PersonalCapital.com or Mint.com to help you organize and understand your finances better. But at the end of the day, you need to establish a budget where you invest in yourself and put 10-20% of your take-home income towards your financial stability and growing your net worth.

Step 2: Build an Emergency Fund - you don’t want to drain your savings to purchase your first home. I recommend having an emergency fund equivalent to 3 months of your living expenses. Again, you won’t know how much this should be if you don’t understand your financial situation and get on a budget as outlined in Step 1.

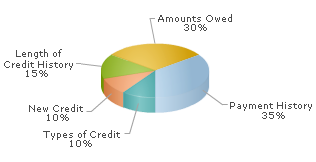

Step 3: Payoff Bad Debt - Any credit card, student loan, car loan, personal loan that you have greater than 8-10% interest, you should try to payoff beforehand. The more your monthly debt payments are, the less mortgage/home you will qualify for. As a rule of thumb, your monthly Debt-to-Gross Income ratio can not be greater than 45%. Meaning if your gross monthly income is $10,000, all of your monthly debt payments including mortgage, property taxes, insurance, can not be more than $4,500. So the less monthly bad debt you have, the easier it will be to qualify for a mortgage. Start with your highest interest balance or the lowest balance and pay it off first and then apply that extra income from debt #1 payment to increased monthly payment on your #2 bad debt loan/credit card. There’s something about being able to get rid of one bad debt first vs. paying a little across all bad debt loans.

Step 4: Save for your home purchase - you are now on your way to becoming an Owner! Most conventional loans require 20% down payment, but if you are a first time homebuyer or veteran, there are programs where you can purchase a home for as little as 3.5-5% down. Meaning if you want to buy a $200k house, you might only need $7k-$10k downpayment vs the conventional loan that would require $40k down payment for a $200k home. Don’t be shy about also asking friends, family, parents to help you achieve Step 4. Rather than holiday, birthday, or wedding gifts, ask your friends to help you with saving for your downpayment. You can get an FHA loan defined by first time homebuyer or if you have not owned a home within the last 3 years for as little as 3.5% downpayment. In some emerging cities the Government has land opportunities called USDA loans where you can get 100% financing! Also, as a first time home buyer, you can take 100% of the downpayment as a gift. Ask your parents to prepay your next 10 yrs of Christmas or Hanukkah and get the ultimate gift of building wealth in real estate this season. Maybe your parents are willing to loan you the money or give you a larger holiday gift in cash! Like anything else, make your goals known and you might be surprised who will help you achieve getting into your first home. There are also some crowdsourcing fundraising out there where friends and family can contribute to your dream of owning a home vs. buying you steak knives! You can get a conventional loan for as little as 5% down. One guideline for financial gifts to achieve your downpayment is that they need to be in your bank account at least 2 months prior to your mortgage funding. There are strict guidelines around tracking your down payment funds, so talk to your realtor or mortgage lender, but crowdsourcing for your downpayment is a great way to accelerate your ability to move from renter to owner.

Step 5: Where would you like to live? - Based on your lifestyle or how far you want to live from your work, start thinking about areas where you want to live and drive the neighborhoods. Do you want to live within a 15 minute commute to your office or within walking distance to restaurants, shops, night life? Most people start with how much house they can afford and then start their search for the biggest home they can buy given their budget. However, you can always update the home, but you can’t take the home out of the neighborhood. So no matter how nice or big the house might be, if you don’t like the area or neighborhood or traffic, you can’t change that. You can remodel the house, but you can’t improve the school district, shopping conveniences, traffic, etc around you. Think about your lifestyle and what are the top 3 things you want in your ideal neighborhood?

Get Started on your Home Buying Process!

Once you’ve narrowed down where you’d like to live, there are a lot of online resources like Zillow and Trulia to give you an idea of home prices in your desired area. It’s about this time you should contact a mortgage broker/lender and see what you can qualify for given your current financial situation, interest rates, etc. You can also contact a local realtor and they can guide you through the process, including mortgage lenders, details about specific neighborhoods, schools, etc. Once you have your mortgage lender and realtor, you have a team to help you move from Renter to Owner - - Congratulations!

Preparing to move from Owner > to > Investor:

Transitioning from Owner to Investor is a big financial milestone, but not as hard as you think with the right team in place (Realtor, Lenders, Attorney, Title). You are approaching a new phase in your journey towards financial stability and building wealth and income through real estate. Very few people achieve this financial milestone and you should be proud to taking this next step. However, just like moving from Renter to Owner, most people ask me, “Where do I start and what’s the next step?” I thought I’d share my experience in how I made the move from Owner to Investor in 2006 and never looked back. It goes like this:

Step 1. Have a clear vision and purpose of why you want to be a successful real estate investor and what your business needs to do for you. Are you looking for short-term gains with flipping houses or long-term cash flow with passive income? Do you want to do this full-time or part-time with property managers and others doing the day-to-day work for you? For my wife and I, our goal was to do this part-time while building long-term wealth via passive income over a 20 yr period. Our goal is to acquire 200+ units generating over $20k+/month (minimum of $100/month positive cash flow per unit) in passive income for our retirement, but a business to also pass on to our children. We are better than 40% along our path to financial freedom, but excited about beating our initial goal of $20k/month positive cash flow. It’s not easy, but again, if you have the right team working with you (realtor, lender, attorney), jointly you will achieve your goals.

Step 2. Build a Great Team. Find great team members to help you pull off your overall vision and purpose. One person alone can only handle so much (and it limits your education). You need a real estate attorney, a realtor, and accountant as a minimum to round out your initial team. If you don’t want to be a property manager, but rather just want checks deposited in your account so you can focus on the next property acquisition, then hire a property manager. Just build this property management expense into your business model which will run you between 6-10% of monthly gross rent. It’s what I do. My goal is to be a real estate investor, not property manager. My current team is one that I’ve built over the past 10 yrs, but consists of a real estate attorney, a broker, 3 agents, 2 property managers, and a handyman. I also have built relationships with 3 different mortgage lenders that I trust and they trust me. Like any business, it comes down to building a great team that trusts one another and understands each other’s role on the team.

Step 3. Know your business model and focus. It's easy to get emotional about a deal, no matter how experienced you are. If you know your numbers and stick to them, it takes the emotion out of the equation. This can save your wallet, big-time. For us, every property has to be cashflow positive from day 1. No Exceptions! Learn to day NO hear and walk away. Or negotiate a deal that meets your positive cash flow from day 1 objective. Meaning, I don’t purchase properties with negative monthly cash flow on a hope of significant future appreciation. My business model is they have to be cash flow positive after all expenses are paid (mortgage, property mgmt, insurance, taxes, etc.) and I can put a plan together to achieve at least 25% annual return on my money after 1 yr. If I can’t make a property perform at this level, then I move on to the next. To be honest, it’s not that difficult to achieve this in real estate, one of the greatest leveraged investments around. As an example, if you invest $20k on a $100k property (20% down), your tenant will pay down about $1300/yr in principle for you and if the home appreciates at the rate of inflation or 3% per year, that’s $3000 in appreciation + $1300 in principle reduction or $4300 gain in the first year. This gives you just over 20% return on your initial $20k downpayment investment. If you are cashflow positive and with depreciation tax deductions, you should be well over 25% annual return on your initial investment of $20k consistently year after year. Compare this to 5-8% in the stock market.

Step 4. Be fanatical about due diligence. Try to obtain and confirm every bit of information you can about an investment — not just the physical property but the history and potential future of revenue, operating expenses, and capital costs. Work with your team to get you the data and put together the numbers to meet your business model or not. That’s why you have a team (realtor, mortgage broker, property manager, etc) to work for you, get you the data, so you can make the investment decision or not.

Step 5. Be a Closer Not a Poser. It only takes a moment to tarnish your reputation. You can’t fake it till you make it. If you can’t close, don’t make an offer. If your plan is to be a long term investor in the area, you’re reputation is bigger than the deal. Be open and realistic with your team. Long-term trust is critical with not just your team, but also your reputation among other realtors, investors, contractors, etc..in the area. If you burn the trust of a contractor, they talk to 10 other contractors, and your next fixer-upper/flip becomes impossible.

Take action! We all have fear when we do something that pushes us out of our comfort zone. The only way around fear is to take action, learn, and educate yourself in the real world. It will be uncomfortable at first, but like anything else, you will become used to it and will most likely get excited about it. I know I did. My wife and I love looking at properties, running the numbers, and envisioning what we can do to improve the property’s financial performance and how it might fit into our long-term vision of passive income and financial stability for our family.